- Why Buy an Existing UK Business in 2026 (Instead of Starting One)

- Types of UK Businesses You Can Buy

- How to Buy a Business in the UK in 7 Steps

- What Does It Cost to Buy a Business in the UK?

- How to Finance a Business Acquisition in the UK

- Due Diligence Checklist for UK Business Buyers

- Common Mistakes UK Business Buyers Make

- Where to Find Businesses for Sale in the UK

Right now, somewhere in the UK, a 63-year-old is trying to work out what to do with the business they've spent thirty years building. They want to retire. Their kids aren't interested. And they're realising that finding the right buyer is harder than they expected.

That's your opportunity, and it shapes how to buy a business in the UK in practice today.

Over 400,000 UK companies with directors aged 60 or over are expected to change hands in the next five years as the baby boomer generation exits — the biggest wave of succession sales the UK has ever seen, and the reason how to buy a business in the UK is on so many professionals' radar in 2026. Combined with improving borrowing conditions and a more transparent marketplace, 2026 is genuinely one of the better years to buy a business in the UK, if you know what you're doing.

This guide walks you through how to buy a business in the UK end to end, from deciding what you want to signing the share purchase agreement, the same process serious buyers use when they buy a business UK-wide in 2026. If you only read one piece on how to buy a business in the UK this year, make it this one. You can browse verified UK businesses for sale on NewOwner while you read, but the steps here apply wherever you source a deal.

Nothing here is academic. These are the actual stages most UK acquisitions go through, the parts that trip people up, and what you can do about it.

Quick tip: Before you look at a single listing, decide whether you're buying a job (owner-operated, day-to-day involvement) or an asset (management-run, absentee-friendly). The two profiles lead to very different shortlists, price expectations, and financing structures.

Why Buy an Existing UK Business in 2026 (Instead of Starting One)

Starting a business sounds exciting. Buying one sounds less romantic. But when you're weighing up how to buy a business in the UK versus building one from scratch, the numbers tell a different story.

Cash flow from day one

When you buy an established business, you inherit its revenue. There's no runway period, no minimum viable product phase, no waiting to see if customers actually want what you're selling. You complete the deal on a Friday, and on Monday you're running a business with existing customers, existing orders, and existing cash flow.

For most acquirers, this is not just convenient. It is how the deal gets financed. Lenders will fund the purchase against the business's own earnings, which means you're borrowing against proven income rather than hoping future income materialises.

Financing is easier for profitable targets

This surprises first-time buyers. Banks and alternative lenders are more willing to back a business acquisition than a startup, because the risk profile is different. An established business with three years of trading history, a customer base, and proven margins is far better loan collateral than a PowerPoint deck.

The British Business Bank's Growth Guarantee Scheme supports SME lending including acquisitions, while challenger banks and asset finance providers have become increasingly active in the UK deal market. You do need to put equity in — 30–50% of the purchase price — but you don't need to fund the full amount yourself.

The demographic succession opportunity

Here is the honest pitch: a lot of what is coming to market right now is genuinely good businesses owned by people who want out. Not distressed assets, not businesses being sold because they're failing. Businesses sold because the owner is 65 and tired, and their accountant told them to sell rather than wind up.

That creates real opportunity. A motivated seller who is not in financial trouble is more likely to offer sensible terms, accept seller financing, and support a proper handover. This is the opposite of a fire sale. It is a succession sale, and those tend to produce better deals for buyers who do their homework.

Types of UK Businesses You Can Buy

Before you start searching, understand the different deal structures and business types you will encounter — this is the foundation of how to buy a business in the UK without tripping over structure later. These affect your tax position, your liability, and your negotiating power. They are not just technicalities.

Share sale vs asset sale

This is one of the most misunderstood parts of buying a business in the UK, and it matters enormously.

When you're planning how to buy a business in the UK, the first choice is between a share sale and an asset sale. In a share sale, you buy the company itself — its shares, and everything that comes with them: assets, contracts, liabilities, staff, HMRC history, and any skeletons in the filing cabinet. You step into the seller's shoes legally. Sellers prefer this structure because it is more tax-efficient for them and produces a cleaner exit.

In an asset sale, you buy specific assets — goodwill, equipment, customer lists, intellectual property — but not the company entity. The seller's limited company stays with them. You're not inheriting historical liabilities, which makes asset sales safer for buyers, particularly where there's any doubt about the company's past.

Most buyers instinctively prefer asset sales for the clean slate. Most sellers instinctively prefer share sales for the tax treatment. The negotiation between these positions shapes many deal structures. HMRC guidance on the tax treatment of each is worth reading before you're in a live deal.

Heads up: Sellers often push hard for a share sale because Business Asset Disposal Relief (BADR) caps their CGT at 14% on the first £1m of gains. Buyers can still agree to this, but should extract matching value elsewhere — tighter warranties, a deeper indemnity basket, or a small price adjustment to reflect the liability risk you're inheriting.

Limited companies, sole traders, partnerships

The majority of businesses sold in the UK operate as limited companies. Some are sole trader businesses or partnerships, which involve an asset purchase by default since there are no shares to buy.

Franchises vs independents

Franchise opportunities sit in their own category. You're buying into an existing brand system with defined operating procedures, and the franchisor will have approval rights over the transfer. Independently owned businesses give you more flexibility to adapt the model but require more independent due diligence on brand, supplier relationships, and competitive position.

Online vs bricks-and-mortar

E-commerce and online businesses have become a sizeable slice of the UK deal market. They have cleaner financials (no lease), transferable customer relationships, and lower overheads. The due diligence looks different though. You are examining domain authority, traffic quality, supplier terms, and platform dependencies rather than a lease and plant equipment.

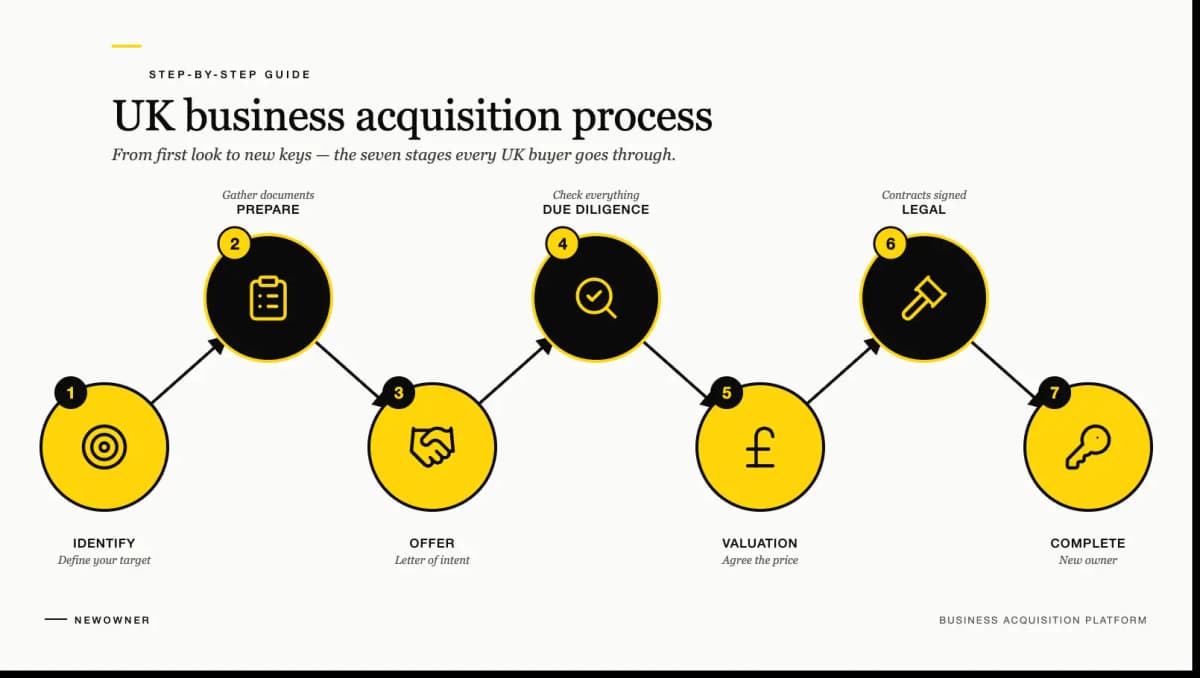

How to Buy a Business in the UK in 7 Steps

Most failed acquisitions go wrong early: wrong type of business, wrong price expectation, or not enough preparation before the first meeting with a seller. Here's how to buy a business in the UK the right way, stage by stage.

Before the steps, here's how the full timeline usually plays out. Every deal differs, but most UK small-business acquisitions follow the cadence below from criteria definition to completion.

| Phase | Typical duration | Key milestone | Main risk |

|---|---|---|---|

| 1. Define criteria | 2–4 weeks | Written buy-box agreed with spouse/partners | Emotional drift onto unsuitable deals |

| 2. Source and screen | 2–6 months | First qualified target under NDA | Wasting time on over-priced listings |

| 3. Valuation and offer | 2–4 weeks | Heads of terms signed | Anchoring on seller's asking price |

| 4. Due diligence | 4–8 weeks | Financial, legal and commercial DD pack complete | Undisclosed liabilities, earnings inflation |

| 5. Financing | 4–8 weeks (parallel) | Formal loan/investor commitments in writing | Lender pulling out late on covenants |

| 6. SPA and completion | 3–6 weeks | Signed SPA, funds flowed | Last-minute warranty and indemnity disputes |

| 7. Handover and first 90 days | 1–3 months | Customer, staff and supplier transitions signed off | Key staff resigning post-completion |

End to end, a typical UK SME acquisition runs 6–12 months from first serious search to completion. Rushing any phase — especially due diligence — is the most expensive mistake buyers make.

Step 1: Define your acquisition criteria

Before you look at a single listing, write down what you're actually looking for. Sector, geography, size range, preferred deal structure, and your personal skills. This sounds obvious, but most first-time buyers waste months looking at unsuitable deals because they didn't rule things out early. For a starting point on which sectors offer the best returns in 2026, see our pick of the 10 best small businesses to buy in the UK.

Be honest about your budget. If you have £200,000 in cash, you can realistically target businesses priced at £400,000–£600,000 (assuming 50% debt financing). Do not get emotionally invested in a £2 million business if you cannot fund it. Limited capital? Read how to buy a business with no money in the UK for seven proven financing structures.

Step 2: Source deals

Most buyers start with the obvious marketplaces. That is fine. It is where a lot of deals are listed. But don't stop there.

Business brokers have off-market deals they share with pre-qualified buyers before listing publicly. Accountants, solicitors, and business advisers sometimes know of clients considering a sale. Direct approaches to business owners in your target sector, done respectfully and professionally, do work.

For listed deals, NewOwner lists verified UK businesses for sale with transparent financials. For a side-by-side breakdown of where deals come from and which marketplace suits which type of buyer, the how to analyse a business before buying is worth reading before you start your search.

Step 3: Initial screening and NDA

When a listing interests you, request the information memorandum (IM) or sales pack. You will need to sign a non-disclosure agreement first. This is standard and reasonable. Read the NDA before you sign it; some are unusually broad.

The IM should give you enough to decide whether to proceed to a call with the broker or seller. At this stage you are not verifying anything. You are deciding if the fundamentals are worth investigating further: sector, location, financials, asking price.

Step 4: Valuation

If the initial conversation goes well, you need to form a view on what the business is actually worth before making any offer.

For most UK small businesses, the primary valuation method is an EBITDA multiple. The UK mid-market average EV/EBITDA multiple sat at 5.3x in H1 2025 (Dealsuite data), but small owner-managed businesses transact at 2.5–5x normalised EBITDA depending on sector and quality.

For a detailed walkthrough of how to value a business in the UK, including which adjustments are legitimate and which ones sellers use to inflate the figure, see the how to value a business in the UK guide. The normalised EBITDA piece matters most. Understanding it puts you in a much stronger negotiating position.

Step 5: Due diligence

This is where most deals either complete or fall apart. Due diligence is your right and responsibility as a buyer to verify everything the seller has told you. It covers financial, legal, commercial, and digital dimensions. We've broken out the full checklist in the section below.

Do not rush due diligence. Sellers sometimes create artificial urgency. 'We have another interested party' is the oldest line in business sales. Take the time you need. The mistakes made here are the ones you live with for years.

Red flag: If a vendor refuses to give you management accounts, VAT returns, or Companies House filings without a signed heads of terms and a non-refundable deposit, walk away. Serious sellers understand that due diligence is non-negotiable. ICAEW's guide to acquisitions sets out the standard documentation pack any UK acquirer should expect.

Step 6: Financing the acquisition

Once you're satisfied with due diligence and have agreed heads of terms, financing is the next pressure point in how to buy a business in the UK successfully. If you're using debt, this is when lenders will want to see the business financials and your own financial position.

If you're exploring creative structures including seller loans or limited initial capital, the how to negotiate a business purchase in the UK covers the options in detail.

Step 7: SPA, completion, and handover

The share purchase agreement (or asset purchase agreement) is the legal document that transfers ownership. Your solicitor drafts or reviews this. It covers warranties, indemnities, completion accounts, and any earn-out provisions.

Completion itself is usually a single day. After that comes the real work: the handover period. How you handle the first 90 days shapes whether the acquisition succeeds or struggles. Staff, customers, suppliers, systems. The post-acquisition transition guide covers that phase in detail.

What Does It Cost to Buy a Business in the UK?

The honest answer to what it costs for how to buy a business in the UK depends enormously on size and sector. A sole-trader van cleaning round might sell for £30,000. A regional accountancy practice might ask £3 million. Here's how to think about price ranges.

| Business size | Typical price range | Implied EBITDA | Multiple range |

|---|---|---|---|

| Micro / lifestyle | £50,000 – £250,000 | £20k – £80k | 2.5x – 4x |

| Small | £250,000 – £750,000 | £80k – £200k | 3x – 5x |

| Lower mid-market | £750,000 – £2,000,000 | £150k – £500k | 4x – 6x |

| Mid-market | £2,000,000 – £10,000,000 | £400k – £2m | 5x – 7x |

Beyond the purchase price, budget for professional fees. A solicitor for a £500,000 business purchase charges £8,000–£20,000 depending on complexity. An accountant to assist with financial due diligence adds another £3,000–£10,000. If you are using a business broker to help you find and structure the deal, their fees vary. Some charge buyers nothing because the seller pays. Others charge a success fee.

Stamp duty on share purchases is 0.5% of the consideration, payable to HMRC via a stock transfer form. That is a relatively small number. Asset purchases may involve SDLT if property transfers, or VAT implications on certain asset categories.

The total cost of acquisition covers the purchase price, professional fees, and any working capital injection the business needs.

How to Finance a Business Acquisition in the UK

Few people working out how to buy a business in the UK have the full purchase price sitting in cash. The good news: several financing routes are available to UK buyers, and lenders have become more active in this market.

Start with your own cash. Most lenders expect 30–50% of the purchase price from your own resources. This "skin in the game" requirement is not negotiable at most banks.

Bank debt covers most of the remainder. Barclays, HSBC, NatWest, and Lloyds all have SME acquisition lending teams. You will need three years of business accounts and a business plan. Rates vary, but expect 6–9% above base on a 5–7 year term.

The British Business Bank Growth Guarantee Scheme offers government-backed lending through accredited lenders that can cover up to 70% of the loan. It is useful where a conventional bank will not go, particularly for smaller deals or buyers without a long credit history.

Start Up Loans let you borrow £500–£25,000 at a fixed 6% annual rate to buy an existing business, with free mentoring included. It will not cover a large acquisition, but for smaller deals it is worth knowing about. The Federation of Small Businesses publishes lender comparison guides that are useful for first-time acquirers.

Seller financing is common in deals below £1 million. Many sellers, particularly those without urgency to liquidate, carry a portion of the price as a deferred payment or loan note. This aligns incentives: the seller wants the business to succeed after handover so they get paid.

Asset finance works if the business has sizeable physical assets. You can potentially refinance machinery, vehicles, or equipment post-completion to release cash against the purchase price.

For ambitious buyers exploring how to buy a business in the UK with a growth story attached, SEIS and EIS structures can bring in investor capital for acquisitions that include a genuine growth element. The Seed Enterprise Investment Scheme and Enterprise Investment Scheme offer tax-efficient ways to raise money.

Most real deals combine two or three of these sources. A typical structure might be 40% buyer equity, 40% bank debt, and 20% seller loan note.

Due Diligence Checklist for UK Business Buyers

Due diligence is the verification phase, and it's the single biggest determinant of whether your plan for how to buy a business in the UK ends well or badly. It is your chance to confirm that what the seller told you is actually true. This is what to cover.

Financial due diligence

- Three years of filed accounts and management accounts (do they reconcile with the filings on Companies House?)

- Aged debtors list. How many customers are overdue, and by how much?

- Aged creditors. What does the business owe, and when is it due?

- VAT returns for the past two years. Does the VAT-reported turnover match the accounts?

- HMRC correspondence. Any open enquiries, penalty notices, or disputes?

- Bank statements for the past three to six months, to verify cash flow against accounts

- Payroll records and employer's NI obligations

Legal due diligence

- All material contracts: customers, suppliers, leases. What are the change-of-control clauses?

- IP ownership: trademarks, domain names, software, patents. Who actually owns them?

- Litigation history. Any current or threatened claims?

- Lease terms: rent, lease break dates, dilapidations liability

- Employment contracts for critical staff, plus any settlement agreements

- Data protection compliance. Is the business GDPR compliant? Any past breaches?

Commercial due diligence

- Customer concentration. What is the top five customers' share of revenue?

- Supplier dependencies. Any single-source supplier arrangements that could be disrupted?

- Critical person risk. Which individuals does the business genuinely depend on?

- Competitive position. Why do customers choose this business over competitors?

- Pipeline. Are there signed contracts or only verbal commitments?

Digital due diligence

- Domain ownership. Is the domain owned by the company or the founder personally?

- SEO traffic. Use Google Search Console access, request it, to verify organic traffic claims

- Social media accounts. Are they owned by the business entity or a personal account?

- Online reviews on Trustpilot, Google, and industry-specific platforms

- Software subscriptions and licences. What transfers, and what needs renegotiating?

For a more detailed framework on reading financial statements and spotting red flags, the how to analyse a business before buying guide goes deeper on the financial and commercial side.

Once you are confident in what you have found, the next step is making an offer and negotiating a purchase price. That has its own set of techniques and common mistakes.

Common Mistakes UK Business Buyers Make

Working out how to buy a business in the UK is a major undertaking, and the same errors come up again and again. Most of them are not exotic. They are predictable and avoidable.

The most common mistake is overpaying because of EBITDA inflation. Sellers sometimes present normalised earnings that include questionable add-backs: owner expenses that would not exist under new ownership, one-off costs that somehow recur every year, or management accounts that do not quite match the filed accounts. The normalised EBITDA guide helps you understand which adjustments are legitimate and which are creative accounting.

Another frequent error in how to buy a business in the UK is ignoring working capital. The purchase price covers the business. It does not necessarily cover the working capital needed to run it. If you complete a deal and the business needs £80,000 in stock or has £60,000 in debtor days, that is cash you need on top of the acquisition cost. Always negotiate a working capital target in the SPA.

Staff retention catches buyers out too. Employees will be unsettled by a change of ownership. Some will leave. Critical staff departures in the first few months can be damaging. They take client relationships and institutional knowledge with them. Think about retention bonuses, communication plans, and whether the outgoing owner stays on for a transition period.

Skimping on warranties and indemnities is another false economy. Warranties are the seller's representations about the business. If they are wrong, you have a claim. Indemnities cover specific known risks. Without them, you bear the cost of anything you did not know about and were not told about. This is not an area to cut legal costs. A good solicitor will protect you.

Finally, moving too fast. The pressure of "there is another offer coming" is real, but manufactured urgency kills discipline. Buyers who rush due diligence to secure a deal find the reason to rush was that the deal needed to be rushed.

Where to Find Businesses for Sale in the UK

If you are working out how to buy a business in the UK today, marketplace coverage matters as much as any single listing. The UK has several active marketplaces for business listings. Each has a different mix of deal types, price ranges, and seller profiles.

NewOwner lists verified UK businesses for sale with transparent financials and a structured acquisition process. It is particularly strong for buyers who want verified information rather than unverified seller claims. You can browse businesses for sale on NewOwner and filter by sector, revenue, and location.

For anyone working out how to buy a business in the UK through public listings, Daltons Business, Rightbiz, and BusinessesForSale.com are the high-volume directories. Thousands of listings, broad sector coverage, varying quality of information. Good for broad market awareness.

Specialist brokers focus on healthcare, hospitality, licensed trade, and professional services. Sector brokers have off-market deals that never reach the general directories. BCMS, Christie & Co, and Hilton Smythe are active in different segments.

A good business broker does more than list. They qualify buyers, manage the process, and know of upcoming listings before they go live.

Direct approaches work too. For a specific business you have identified, a respectful direct approach to the owner sometimes works. Be professional, be direct about your interest, and do not lowball in an opening approach.

For a full breakdown of which marketplace suits which buyer profile, the how to analyse a business before buying covers the main differences.

Whichever route you use, verify independently. Listing information is provided by sellers, not verified by marketplaces as standard. The due diligence phase is your check on everything you have been told.

Worth knowing: When you're working out how to buy a business in the UK, sourcing is typically the easy part. Over 400,000 SMEs will change hands this cycle. The scarce skill is disciplined valuation and a due-diligence process you refuse to skip under seller pressure. Every successful buyer we speak to says the same thing: how to buy a business in the UK is really a question about how slowly you can stay during due diligence, not how fast you can close. Take that lesson forward, and the rest of the process falls into place.

Ready to sell your business?

Get Started